Key Takeaways

- You should ready your finances, lifestyle, and expectations before starting your home search.

- A mortgage pre-qualification helps define your budget, while a mortgage pre-approval strengthens your offer.

- Understanding each step of your homeownership journey helps you move with confidence.

Step 1: Make Sure You’re Ready to Buy a Home

Before exploring listings or mortgage calculators, ensure that your finances, lifestyle, and expectations align with the realities of homeownership. A home is a long-term commitment, so ensure you’re comfortable with everything from upkeep to basic maintenance.

- Stable income and employment are key as mortgage lenders look for consistency.

- Debt levels should be manageable, allowing you to afford your monthly payments.

- Upfront costs include more than just your down payment (think home inspections, legal fees, and closing costs)

- Ongoing costs, such as property taxes, maintenance, condo fees, utilities, and repairs, can quickly add up.

Step 2: Organize Your Finances and Build Your Budget

Understanding what you can afford makes your home search much smoother. A 20% down payment avoids default insurance, but it’s not mandatory unless your home price is $1.5 million or more.

- Use tools like nesto’s mortgage affordability and mortgage payment calculators to estimate your monthly costs.

- Understand your debt service ratios (GDS and TDS), which help mortgage lenders determine your eligibility for a mortgage.

- Begin saving for a down payment (5% is the minimum in Canada, depending on purchase price) and closing costs (between 1% and 4%).

- Consider support from programs like the Home Buyers’ Plan (HBP) and the First Home Savings Account (FHSA).

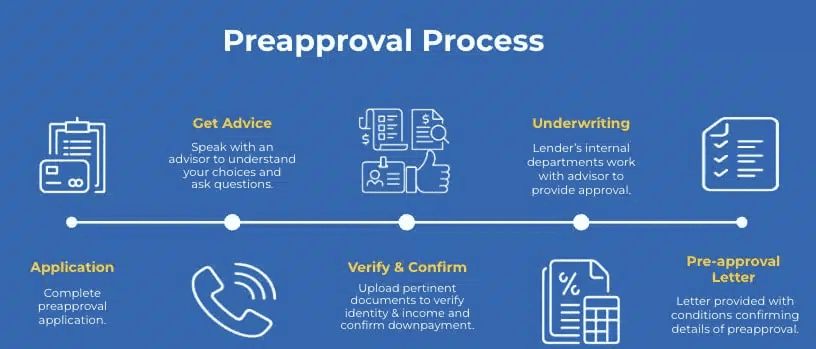

Step 3: Get Pre-Approved for a Mortgage

A mortgage pre-approval gives you a clear picture of what you can afford and shows sellers you’re a serious buyer. While it’s not a final approval, it sets the stage for a smoother, more confident homebuying experience. If you’re just getting started, a mortgage pre-qualification can be a helpful first step to understand your expectations and borrowing potential.

Work with mortgage brokers to review your options, receive personalized advice, and gather the necessary documents to proceed with your mortgage application. Once approved, you’ll receive a letter stating the amount you can borrow and a rate hold (usually valid for 90 – 120 days).

You’ll need to gather your required mortgage documents, such as:

- ID and proof of income

- Pay stubs, T4s, or self-employed income docs

- Debt and asset info

- Down payment source details

Step 4: Start Your Home Search

Now it’s time to work with a trusted real estate agent and look for properties that match your needs and budget. Always check recent sales in the area and consider a home inspection, especially for older properties or detached homes.

What to Consider:

- Location: Commute time, schools, and access to amenities and transit.

- Property type: House, condo, or townhouse (each has its pros and cons).

- Ownership structure: Freehold, condo, or co-op (each has its pros and cons).

- Condo fees: If applicable, these will increase your monthly expenses and impact your mortgage approval amount.

- Property taxes: This will increase monthly expenses and affect the mortgage amount you qualify for.

- Home inspection: Consider completing a home inspection before waiving your finance conditions.

- Potential repairs: If a full appraisal is required, any significant renovations or repairs could impact your approval.

Step 5: Make an Offer

Once you’ve found a home that feels like the right fit, the next step is to move forward with making an offer and beginning the homeownership process. Ensure your mortgage approval is solid and that you’re comfortable with any financing conditions on your purchase before waiving them.

- Work with your realtor to submit an offer with conditions (such as financing, inspection, etc.).

- Provide a deposit (to your realtor’s trust account) once your offer is accepted, usually 1–5% of the purchase price.

- Be ready to negotiate terms and conditions through your realtor, such as price, closing date, and inclusions.

- Once accepted, the offer becomes a binding agreement

- Now work with your mortgage lender to firm up your mortgage approval (this includes due diligence on the subject property).

- Secure your property insurance, as your lawyer or notary will need to see that it’s in place on your closing day.

Step 6: Prepare for Closing Day

Closing is when ownership officially changes hands, and many things need to align. Your mortgage lender will send instructions to coordinate with your lawyer or notary to finalize the transaction, register the title, and transfer the funds.

Step 7: Move In and Settle Into Homeownership

Step 7: Move In and Settle Into Homeownership

Once you’ve got the keys, your homeownership journey begins. If you used incentives like the Home Buyer’s Plan or other programs, keep track of any repayment timelines. Here’s what you’ll need to manage:

- Update your utilities and notify all relevant parties, including the Canada Revenue Agency (CRA), if this will be your primary residence.

- Set aside a repair fund for unexpected issues

- Start making regular mortgage payments

- Review your budget regularly as a homeowner; keep spending, saving, and household funds separate to make it easier to manage your budget.

First-Time Buyer Programs That Can Help

You can combine multiple first-time homebuyer programs as long as you meet the eligibility requirements of each program. For example, if you buy in Toronto, you can receive both the provincial and municipal land transfer tax rebates for a total rebate of $8,475. You can also take advantage of all other programs like the HBP, FHSA, and any other tax credits and rebates to boost your savings.

Here’s a quick look at the top federal and provincial programs that may reduce your costs:

Final Thoughts

Buying your first home might seem overwhelming, but it doesn’t have to be. With the customized guidance and a clear plan, the path to homeownership becomes much easier to follow. When you understand each step, from budgeting to making an offer, you can move forward with confidence and clarity.

If you’re ready to explore your home financing options or just want honest advice to help you get started, nesto mortgage experts are here to guide you through every part of your homeownership journey. Let’s make your first home purchase easier and simpler.